EMI × Kohler · Marketplace Intelligence

Kohler Indonesia

Home & Living Marketplace Review

Shopee & Tokopedia · January–April 2026

An executive synthesis of category performance, Kohler's competitive position, brand differentiation and the outlook — built from EMI's monthly decks and SKU-level marketplace data. Every figure is click-to-source.

Executive Summary · Market Size · Kohler Share · Trends & Platform · Growth vs Market · Competitive Landscape · Differentiation · 6-Month Outlook · Action Plan · Sources

01 · Executive Summary

The five things to know

- Kohler is rank #6 in Indonesia — a premium niche in a value-led market. ~5.5% share of the tracked sanitaryware competitive set in April, behind local volume leader Onda (~37%), Toto (~20%), Paloma (~13%), Europe Enchanting (~12%) and American Standard (~6%). Rank has held at #5–6 all four months. source

- The market is large but value-skewed, and Onda dominates. The category turns over ~Rp 95–117bn/month, but ~28% is unbranded/generic and the median product sells for only ~Rp 48,500. Onda alone is over a third of the tracked premium set and is still gaining (+6.4pp Jan→Apr). source

- Kohler is genuinely premium-positioned — the opposite of a discount play. Its weighted ASP (~Rp 1.1M) is the highest in the set, and it over-indexes the top tier: 15% of Kohler's sales are above Rp 8.5M vs just 3% for the set. Premium positioning is visible here. source

- But Kohler is drifting, not climbing. Sales fell ~17% Jan→Apr (−0.7pp share) while the set's value tier reshuffled — Paloma collapsed (−7.3pp) and Toto slipped (−2.1pp), vacating demand Kohler did not capture. And Kohler discounts deepest in the set (~31%) despite its premium price. source

- Hero-SKU presence is the gap. Kohler has zero products in the set's top-30 bestsellers (Onda has 16, Toto 6). Its range is diversified — showers/sprays, toilets, faucets, basins — but thinly spread, with only one genuine volume product (the PureWash portable bidet spray). source

- The market is moving Kohler's way — if it acts. External research (Aissistance Deep Research) confirms an expanding middle class and ~20M "power consumers" shifting to international prestige brands, a government housing-VAT stimulus running to 2027, and a Tokopedia–TikTok Live-commerce channel for premium discovery. The premium upgrade cycle — not Onda's price floor — is Kohler's route. This reframes the action plan below. EXT ↗ research

02 · Market & Category Size

A ~Rp 380bn category, Shopee-led and value-skewed

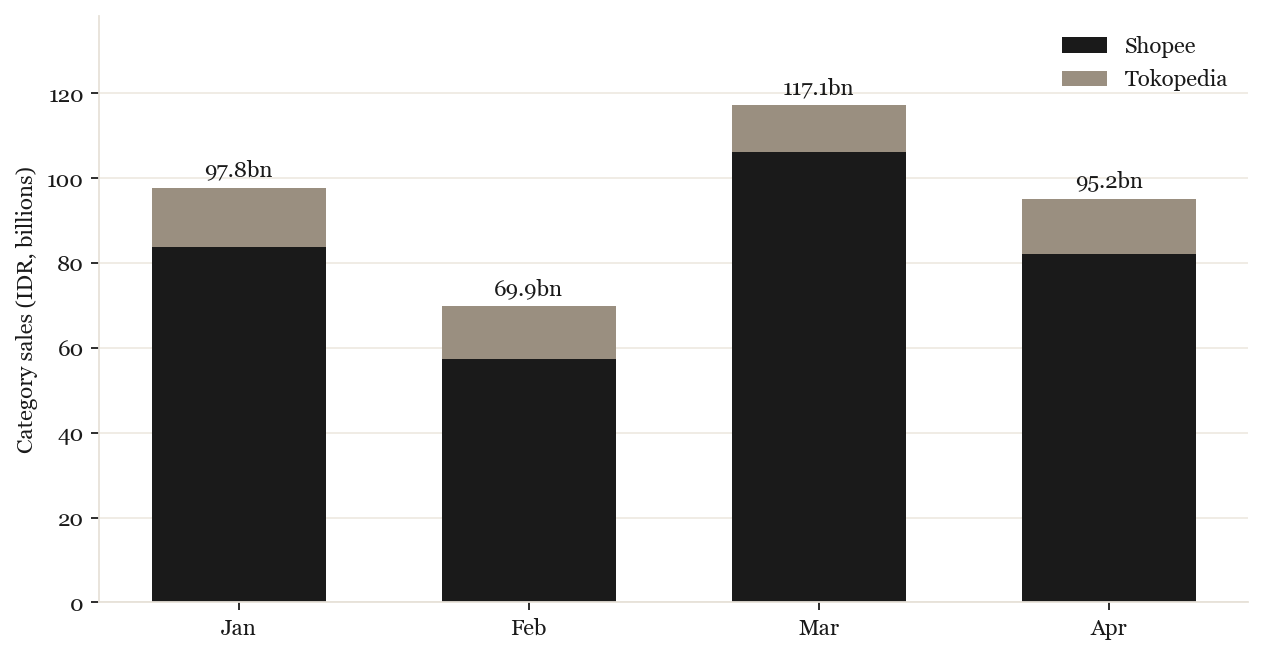

Indonesia's Home & Living category on Shopee + Tokopedia turned over roughly Rp 380bn in Jan–Apr 2026 (~Rp 70–117bn per month). Shopee is ~86% of it.

April category sales were ~Rp 95bn. An important caveat for interpretation: ~28% of the total is unbranded or generic merchandise and the median item sells for only ~Rp 48,500 — this is a price-driven mass market. Kohler's competitive arena is the tracked sanitaryware brand set (~Rp 18–29bn/month), used throughout the rest of this report. source: deck source: data

Category sales by month, split by marketplace (all listings). Derived from EMI × Kohler ID raw data, Jan–Apr 2026.

03 · Kohler Market Share & Position

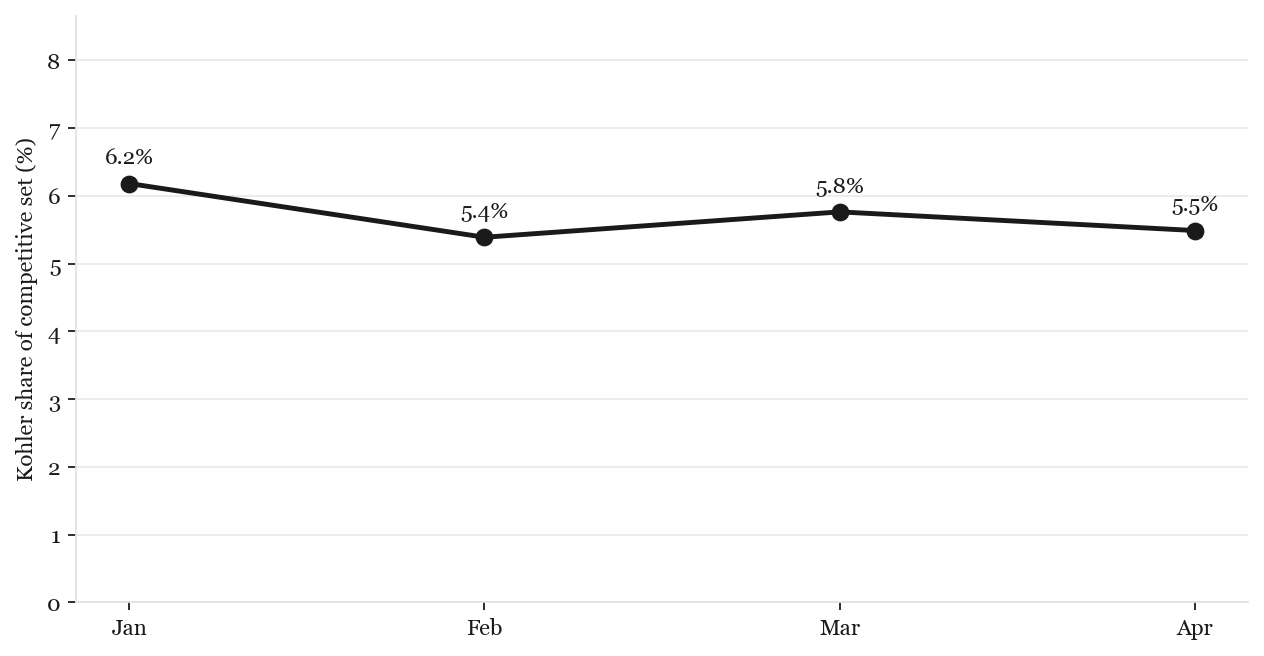

#6 in the arena — a stable but stalled premium niche

Within the tracked sanitaryware set, Kohler has held a narrow band — 6.2% (#6) in January, a brief #5 in March, settling at 5.5% (#6) in April. It sits behind a clear top five: Onda (37%), Toto (20%), Paloma (13%), Europe Enchanting (12%) and American Standard (6%). source

Among Official-store sales specifically, Kohler holds ~5.6% in April — in line with its overall set share, so the brand is not yet over-indexed in the Official channel and has room to build a stronger, brand-controlled premium position.

Kohler share of the tracked sanitaryware competitive set, by month. Scope & method: see RECONCILIATION notes.

04 · Category Trends & Platform

Shopee leads the category — but Tokopedia carries the premium set

Shopee is ~86% of the overall category. But within the tracked premium set the split is very different: in April the set ran Rp 14.7bn on Shopee vs Rp 8.6bn on Tokopedia — Tokopedia is ~37% of the branded arena, far above its ~14% of the headline category. Premium sanitaryware buyers over-index on Tokopedia, making it a more strategically material channel than the topline suggests. source

Platform split by month, Jan–Apr 2026 (all listings).

The longer view — 13-month trend & seasonality

The EMI deck's 13-month rolling trend shows a category running well above last year, with month-to-month volatility (a soft February, a March peak, an April easing). The April dip is a seasonal fluctuation rather than a reversal. (Click the source tag to view the EMI deck's 13-month trend slide.) source

05 · Kohler vs Market Growth

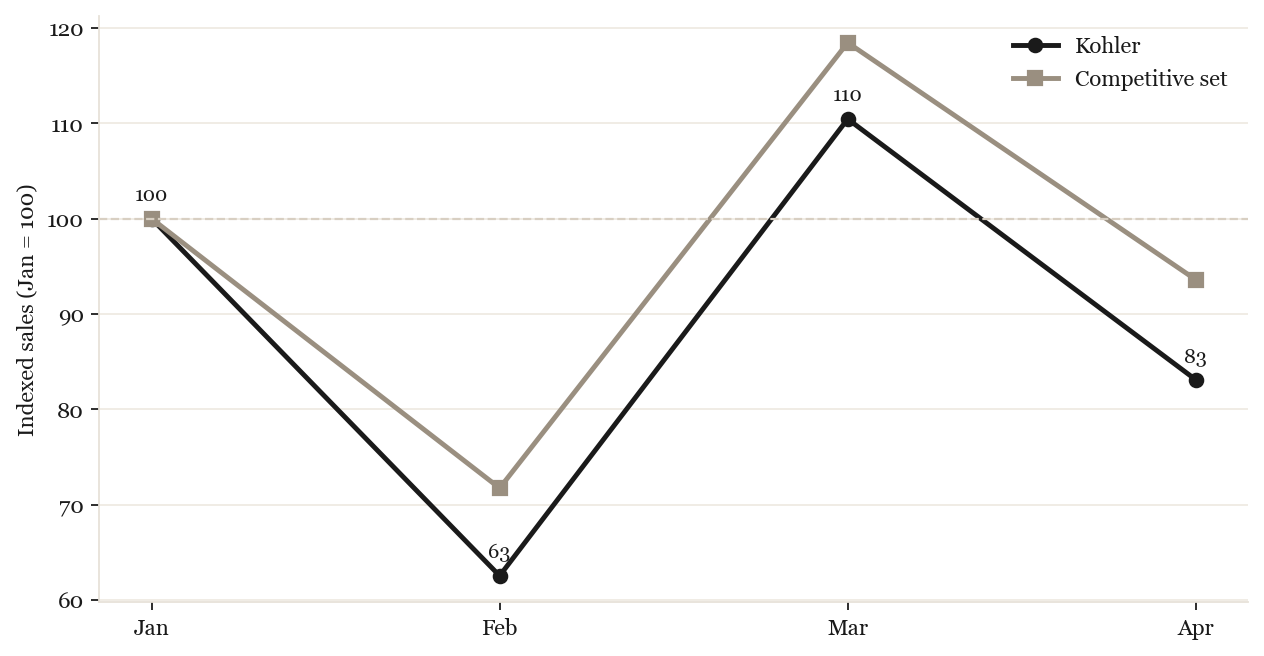

Tracking the market down — and underperforming it in April

Indexed to January, Kohler broadly followed the competitive set's choppy path (soft Feb, March peak), but ended April below it — Kohler at 83 vs the set at 94. Kohler's ~17% sales decline Jan→Apr is steeper than the set's, and steeper than the leaders who gained. The brand is not yet converting its premium positioning into momentum. source

Monthly sales indexed to January = 100, Kohler vs the competitive set.

06 · Competitive Landscape

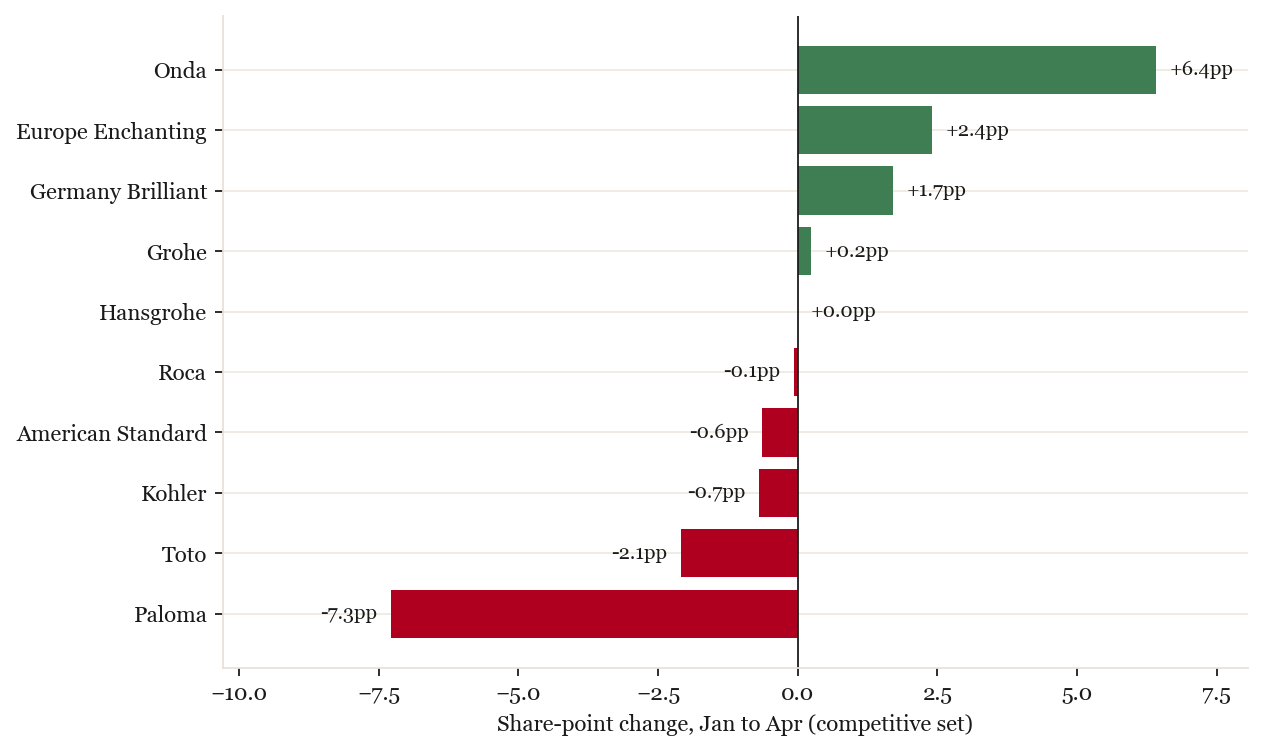

Onda owns volume; the value tier is reshuffling

Local champion Onda dominates (~37% and still gaining +6.4pp), built on cheap, high-volume product (ASP ~Rp 167k). The big shifts are in the value/mid tier: Paloma collapsed (−7.3pp, −40% sales) and Toto slipped (−2.1pp), while Europe Enchanting (+2.4pp) and Germany Brilliant (+1.7pp, +47% sales) rose. Kohler held roughly flat (−0.7pp) — neither winning the vacated demand nor losing badly. source

April competitive-set ranking

| Brand | Apr sales (Rp bn) | Share | Δ share (Jan→Apr) |

|---|---|---|---|

| Onda | 8.5 | 36.7% | +6.4pp |

| Toto | 4.7 | 20.4% | −2.1pp |

| Paloma | 3.0 | 12.8% | −7.3pp |

| Europe Enchanting | 2.8 | 12.2% | +2.4pp |

| American Standard | 1.4 | 5.8% | −0.6pp |

| Kohler | 1.3 | 5.5% | −0.7pp |

| Germany Brilliant | 1.1 | 4.7% | +1.7pp |

| Grohe | 0.4 | 1.7% | +0.2pp |

Tracked sanitaryware set, April 2026. Full Top-10 brand detail by platform is in the deck. Shopee Top 10 Tokopedia Top 10

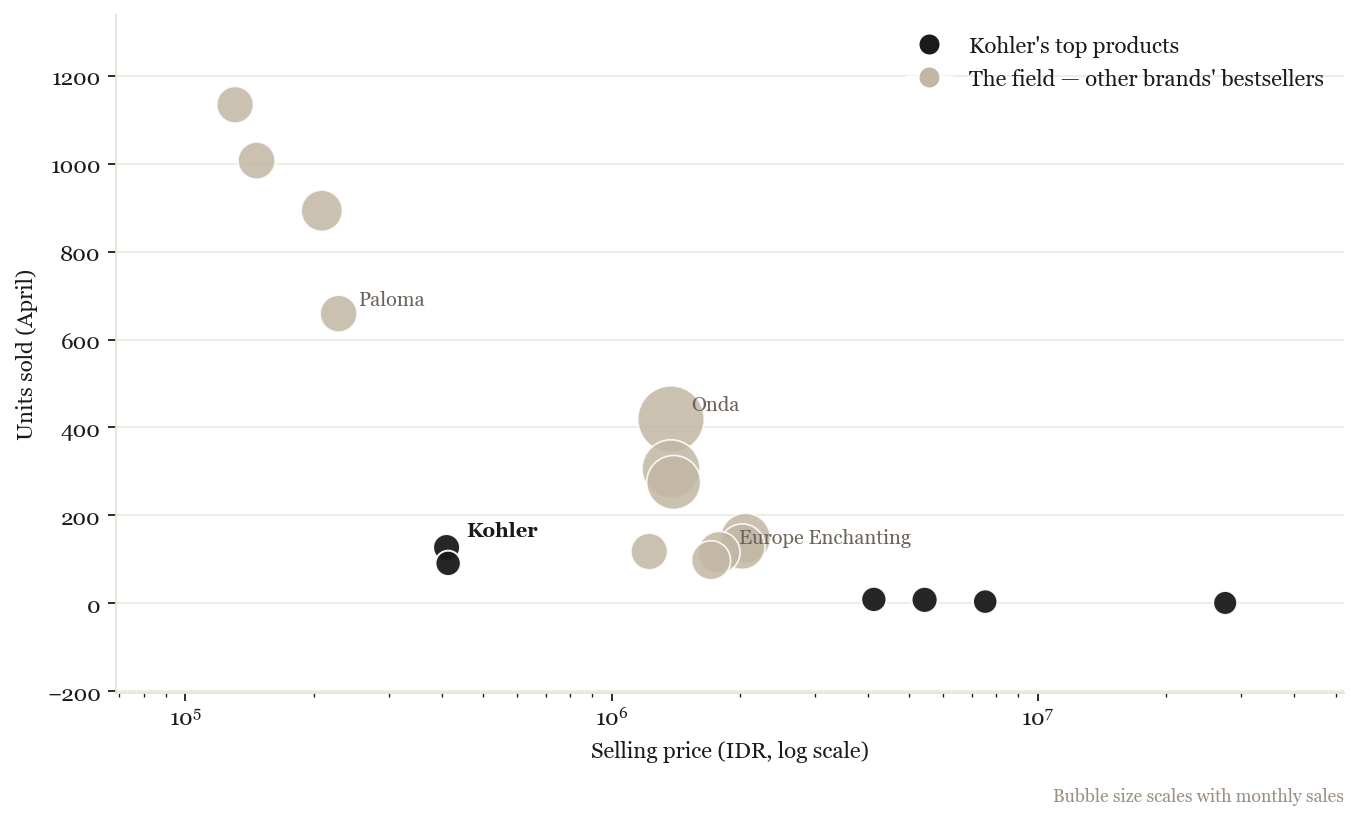

What's winning — and where Kohler sits

The bestseller list is dominated by local value brands: Onda alone holds 16 of the top 30 products, with Toto (6), Paloma (4) and Europe Enchanting (3) filling most of the rest. Kohler has zero products in the top 30. Its bestsellers sit at higher price points and lower volumes — premium, but without a breakout hit. Bubble size = monthly sales. source deck SKUs

Kohler's bestsellers — one volume product, then premium

Kohler's top products are anchored by a single genuine volume item — the PureWash portable bidet spray (~Rp 410k, 127 units) — followed by premium shower columns (Rp 4–7.5M, single-digit units) and a Rp 27.5M Whitehaven kitchen sink. The pattern: a strong accessory beachhead plus a thin premium tail, with little in the high-volume mid-market that Onda and Paloma own. source

| Kohler product | Price Rp | Units | Sales Rp M |

|---|---|---|---|

| PureWash portable bidet spray | 410k | 127 | 51 |

| Taut shower column set | 5.43M | 8 | 43 |

| PureWash portable bidet spray (jet) | 414k | 91 | 38 |

| Atom shower column set | 4.13M | 9 | 37 |

| July shower column (thermostatic) | 7.53M | 4 | 31 |

| Whitehaven undermount kitchen sink | 27.5M | 1 | 28 |

07 · Brand Differentiation

Channel, assortment & pricing

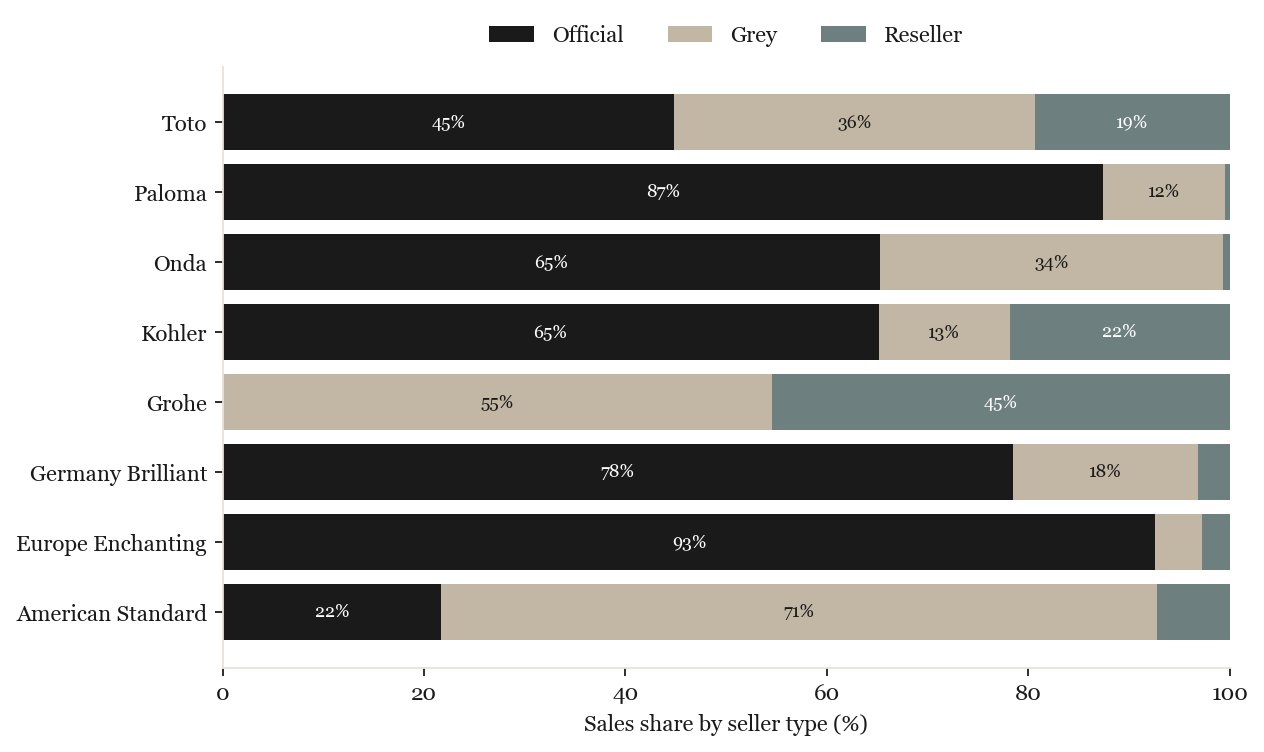

Channel — Official-led, but with leakage

65% of Kohler's sales flow through Official stores, with 22% via resellers and 13% grey-market — solid but not best-in-class. Europe Enchanting (93%), Paloma (87%) and Germany Brilliant (78%) run tighter Official operations; American Standard (22%) and Grohe (0% Official) are far looser. Tightening Kohler's channel control is a structural edge only partly realised. source

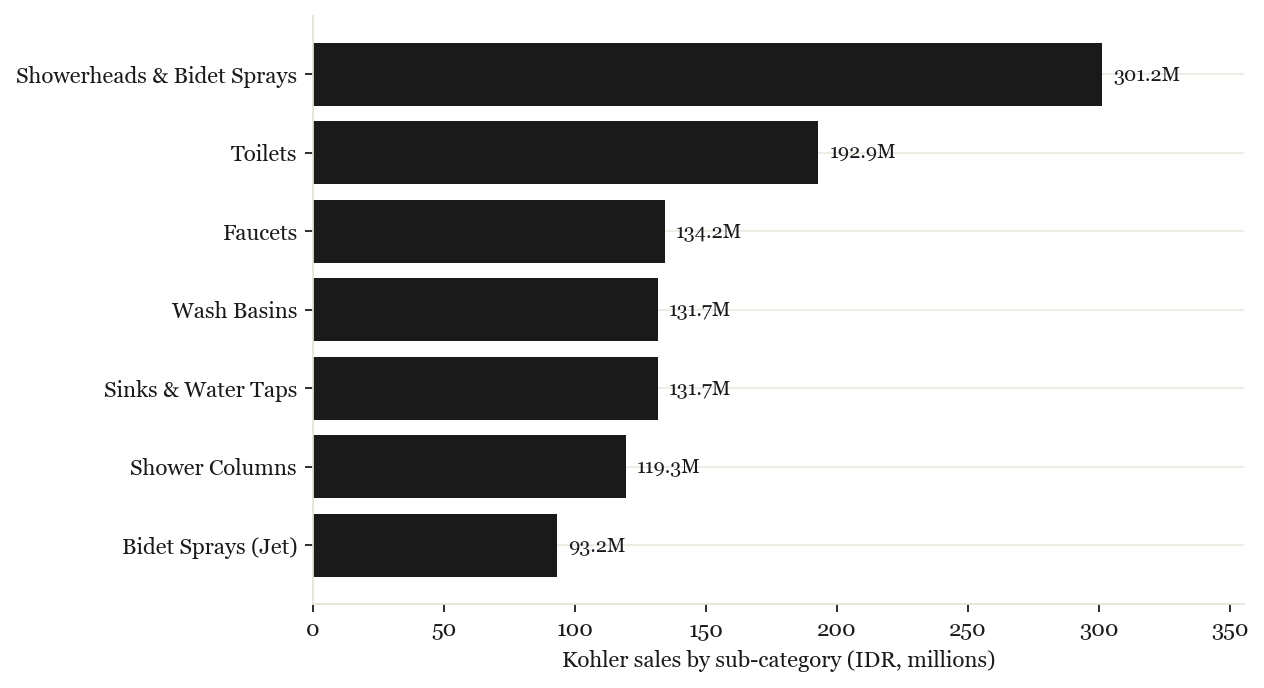

Where Kohler plays — diversified, led by showers & sprays

Kohler's Indonesia range is genuinely broad: Showerheads & Bidet Sprays (Rp 301M) leads, followed by Toilets (Rp 193M), Faucets, Wash Basins and Sinks (~Rp 130M each), plus shower columns. Unlike a showers-only play, Kohler has a real toilet presence here — but no single category is built into a volume engine. source

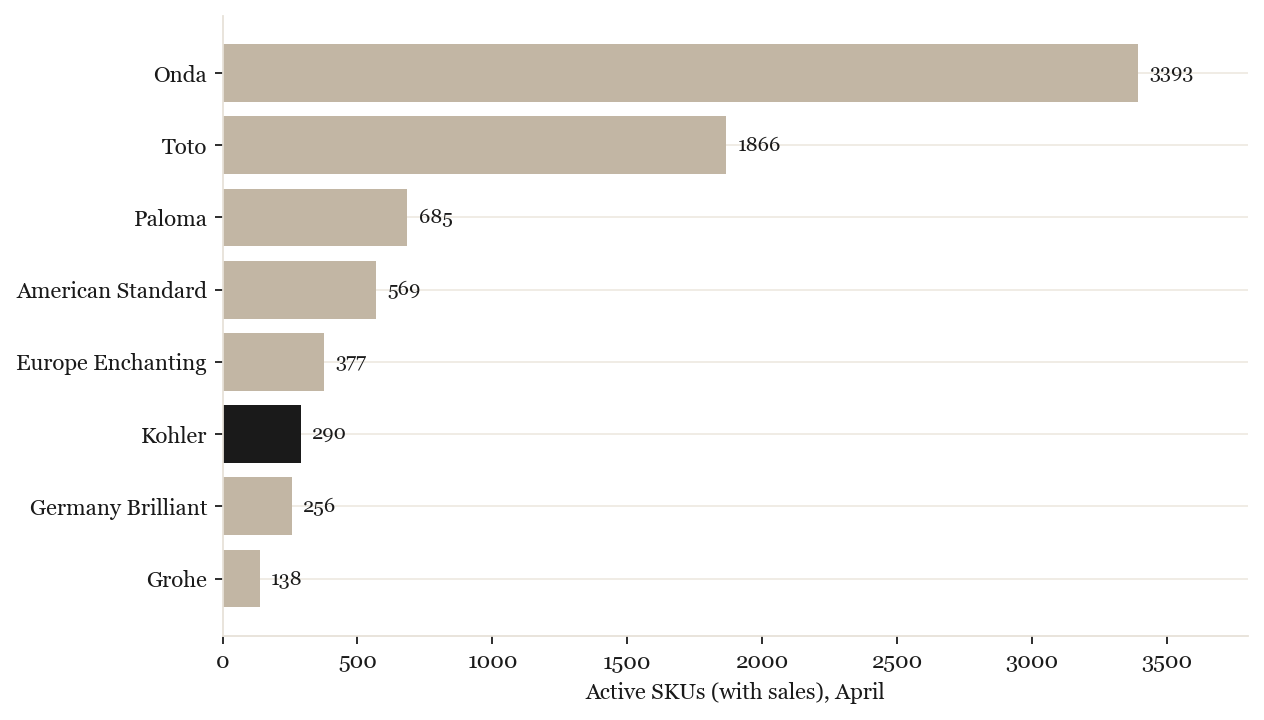

Assortment — narrow vs the volume leaders

Kohler sells through 290 active SKUs — far below Onda (3,393) and Toto (1,866), and below Paloma (685) and American Standard (569). It is a focused range, but thin shelf presence against brands carrying 5–10× the listings. source

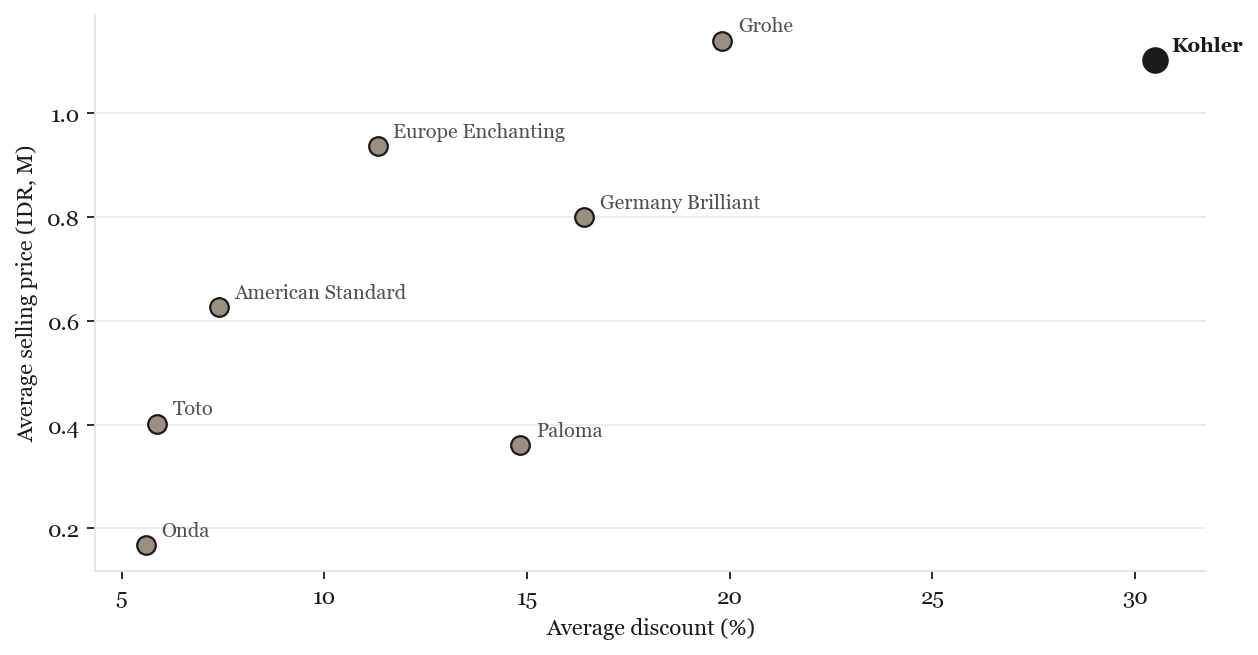

Pricing — premium price, but deepest discount

Kohler's ~Rp 1.1M ASP is the highest in the set, confirming a premium position. The concern: a ~31% average discount — the deepest of any brand (most rivals 6–20%). Kohler is signalling premium on price but undercutting it on promotion. source

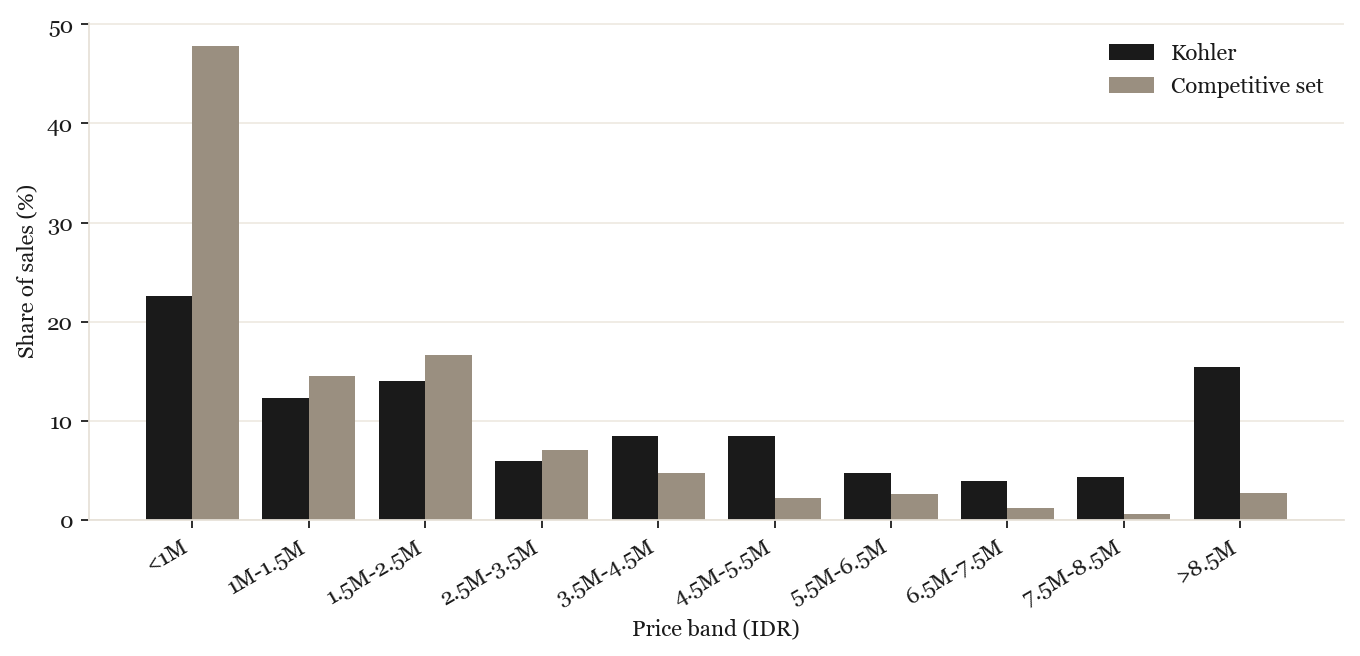

Pricing tier — Kohler genuinely owns the top end

Across price bands Kohler skews premium: 15% of its sales are above Rp 8.5M vs just 3% for the set, and it under-indexes the <Rp 1M mass tier (23% vs the set's 48%). This is the inverse of a value-brand profile — a real asset to build on, provided it is matched with hero SKUs and channel discipline rather than blanket discounting. source

Promotion & listing quality

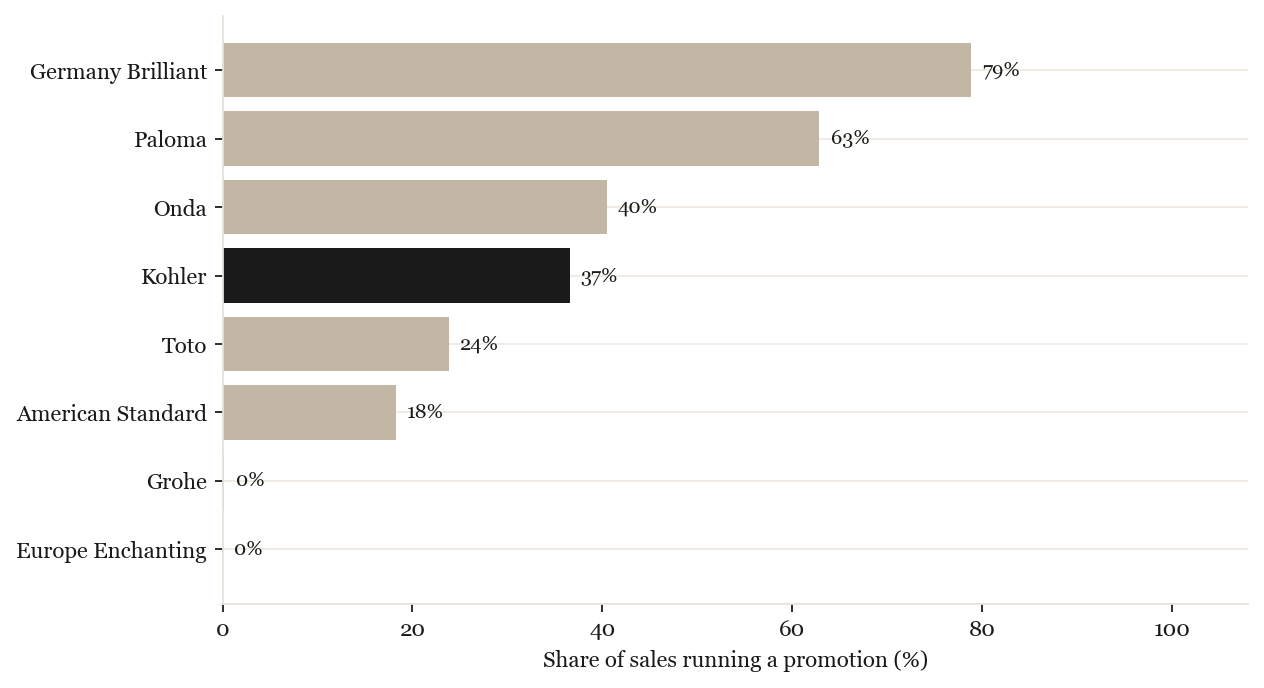

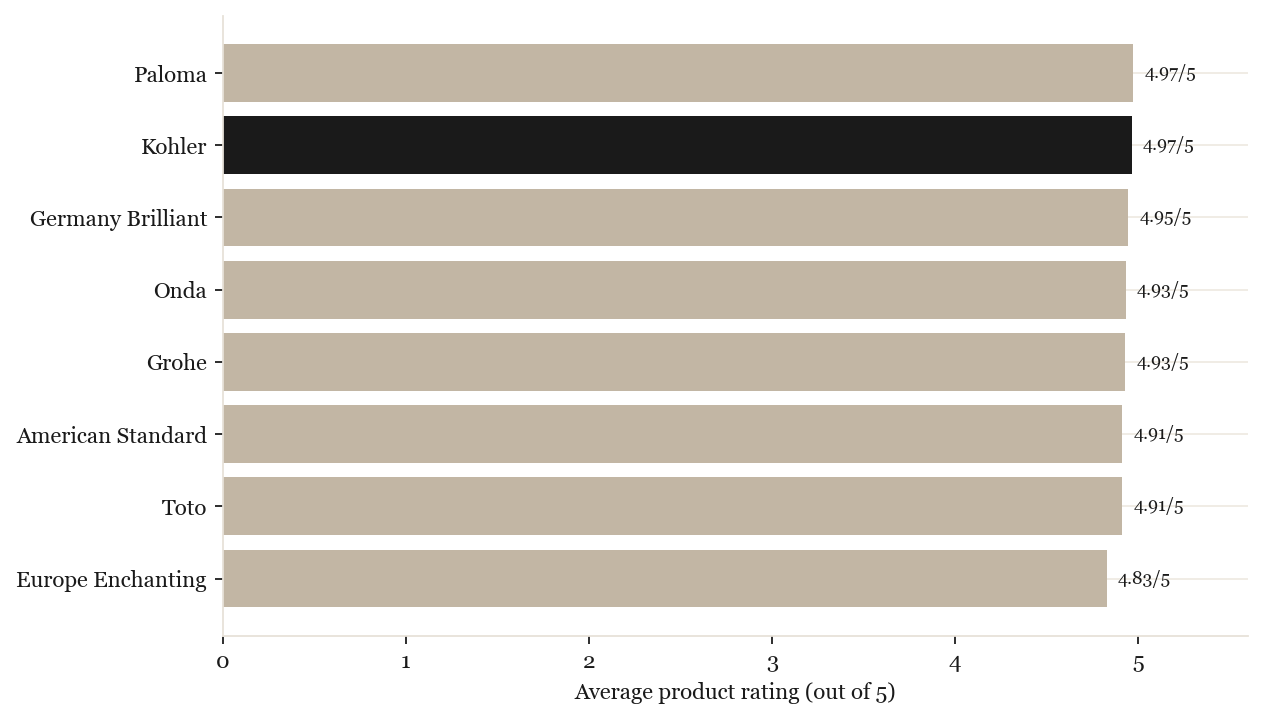

Encouragingly, Kohler runs only 37% of sales on promotion — more disciplined than Germany Brilliant (79%), Paloma (63%) and Onda (40%) — so the deep average discount is concentrated, not universal. On product ratings every brand clusters at ~4.9/5 (Kohler joint-highest at 4.97), so listing quality is table-stakes, not a differentiator. source: promo source: quality

08 · Six-Month Outlook

Where the next two quarters point

Directional calls grounded in the 4-month trajectory and the deck's 13-month seasonality. Ranges are indicative, not forecasts — only ~13 months of history exist.

| Theme | Direction | Read |

|---|---|---|

| Category demand | ↑ (choppy) | Category runs well above last year with monthly volatility; expect seasonal swings around a rising trend rather than a sustained decline. |

| Kohler set share | →/↓ unless acted on | On current trajectory Kohler drifts at ~5–6%. Upside to ~7–8% is available if it converts premium positioning into hero SKUs and captures Toto/Paloma's vacated demand. |

| Competitive risk | watch | Onda keeps gaining at the volume floor; Europe Enchanting and Germany Brilliant are rising in the mid-premium tier where Kohler should be strongest. |

| Margin quality | watch | A 31% average discount on a premium ASP is the key vulnerability — it erodes the premium signal Kohler otherwise earns on price and assortment. |

Seasonality & long-horizon basis: EMI deck 13-month trend & MAT. source

External signals — forward-looking context

Surfaced by Aissistance Deep Research; treat as forward-looking signals rather than already-realised changes in our April data.

| Signal | Type | Read & implication for Kohler |

|---|---|---|

| Expanding middle class & ~20M "power consumers" | tailwind | An upgrading middle class is shifting toward international prestige brands — the structural tailwind behind a premium pivot away from Onda's price floor. EXT ↗ |

| Government housing VAT stimulus (PPN-DTP, to 2027) | tailwind | New-homeowner demand for full-bathroom outfitting — a defined, time-boxed campaign window for bundles. EXT ↗ |

| Tokopedia–TikTok Shop & Live commerce | opportunity | A new premium-discovery and shoppertainment channel; first-mover "Live" demonstration of premium product builds equity the static listing can't. EXT ↗ |

| Smart-toilet / electronic-bidet shift | watch / opportunity | Demand is moving from manual sprays to electronic bidet seats; Kohler must elevate its smart offering or cede the upgrade cycle to challengers. EXT ↗ |

09 · AI Action Plan

Nine moves — marketplace data sharpened by external research

The marketplace data drove six initial moves; an external Aissistance Deep Research pass confirmed the premium-pivot thesis and surfaced three new fronts. The central message: Indonesia rewards a premium upgrade play, not a price war with Onda — an expanding middle class and ~20M "power consumers" are shifting toward international prestige brands, and the win comes through hero SKUs, Tokopedia/Live-commerce discovery, O2O and the project channel. EXT ↗ Full research

1 · Anchor authenticity in the Official Store

82% of shoppers rely on reviews to mitigate the "sensory gap" on high-ticket items — the Official Store is the trust anchor against a 28% unbranded market. EXT ↗2 · Tighten the channel (65% → higher)

65% Official with 22% reseller / 13% grey leaves leakage; peers run 87–93%. Enforce pricing/MAP.3 · Build hero SKUs in showers & bidet sprays

"Mandi" hygiene culture demands water-hygiene products; market the Cuff/Luxe sprays as entry points and elevate electronic bidet seats. EXT ↗ EXT ↗4 · Tokopedia + Live-commerce discovery

The Tokopedia–TikTok Shop merger created a premium-discovery paradigm; build a "shoppertainment" Live-commerce strategy, not just Shopee depth. EXT ↗ EXT ↗5 · Capture vacated premium demand

Paloma (−7.3pp) and Toto (−2.1pp) are slipping; conquest the mid-premium tier where Kohler fits.6 · O2O "webrooming"

Drive online browsers to Kohler Experience Centers and premium retail (Mitra10, Depo Bangunan) to close the sensory gap on intelligent toilets. EXT ↗7 · Target the housing VAT stimulus

The PPN-DTP housing incentive runs to 2027 — build "New Homeowner Bundles" (basin + faucet + toilet + spray) for full-bathroom outfitting at handover. EXT ↗8 · E-commerce data → B2B leverage

Use online search velocity, wish-lists and reviews as proof of brand desirability to win developer specification at IndoBuildTech. EXT ↗Detail & rationale

- Anchor authenticity in the Official Store. External research finds 82% of Indonesian shoppers rely on reviews to build trust on high-ticket purchases. The Official Store is Kohler's critical authenticity anchor against the 28% unbranded/generic share — make reviews, warranty and genuineness unmistakable. source EXT ↗

- Tighten the Official-store channel. 65% Official with 22% reseller and 13% grey leaves room — peers like Europe Enchanting (93%) and Paloma (87%) run tighter. Enforce pricing/MAP and reduce grey-market leakage to protect brand equity. source

- Build 3–5 hero SKUs in Showerheads & Bidet Sprays. Already Kohler's #1 sub-category (Rp 301M) and the PureWash spray proves Kohler can win volume — yet it holds zero of the set's top-30. Indonesia's "Mandi" bathing culture demands robust water hygiene: market the Cuff/Luxe hygiene sprays as accessible entry points and elevate electronic bidet seats for the post-COVID hygiene shift. source EXT ↗ EXT ↗

- Invest in Tokopedia and Live commerce, not just Shopee depth. The premium set already draws ~37% of sales from Tokopedia (vs ~14% of the headline category), and the Tokopedia–TikTok Shop merger has created a powerful premium-discovery channel. Build a "shoppertainment" Live-commerce strategy to demonstrate product superiority across both platforms. source EXT ↗ EXT ↗

- Capture the premium demand Toto and Paloma are vacating. Paloma lost 7.3pp and Toto 2.1pp of set share Jan→Apr. Conquest those mid-premium buyers — where Kohler's price and quality already fit — rather than chasing Onda's mass-volume floor. source

- Rationalise discounting to protect the premium signal. Kohler runs the deepest discount in the set (~31%) on the highest ASP. Promotions should pivot permanently to value-adds (free installation, bundling) rather than margin erosion that destroys luxury equity. source

- Launch a unified O2O "webrooming" strategy. High-ticket items suffer cart abandonment because buyers cannot physically inspect them. Use e-commerce as a high-fidelity digital catalogue that explicitly drives shoppers to Kohler Experience Centers and premium retail partners (Mitra10, Depo Bangunan) to close the sensory gap on intelligent toilets and premium suites. EXT ↗

- Target the government housing stimulus. The PPN-DTP (VAT) housing incentive is active through 2027. Build digital campaigns and "New Homeowner Bundles" (basin + faucet + toilet + spray) to capture full-bathroom outfitting at the point of property handover. EXT ↗

- Turn e-commerce data into B2B leverage. The developer pipeline dictates mass volume. Use online search velocity, wish-list additions and positive SKU reviews as empirical proof of brand desirability — and present that B2C engagement data at trade shows like IndoBuildTech to win developer specification contracts. EXT ↗

10 · Sources

Every insight, traced

Click any insight's “source” tag above, or any thumbnail below, to view the underlying slide or chart. Derived charts are computed from EMI × Kohler ID SKU-level data (Jan–Apr 2026, Shopee + Tokopedia); deck pages are from the EMI × Kohler ID April 2026 report.

External research

Aissistance Deep Research, 3-pass run (June 2026). Each item below links out to the cited source

in a new tab. The full merged research file (100+ sources) is at

report/research/id_external_context_merged_20260618_121158.md.

EXT ↗ Full merged report